银行股Q3季报:JPMorgan目标价$100, Goldman Sachs关注Tangible Book Value 价值投资者2022-10-18 20:33:04

Q3 may offer JPMorgan at $100 and Goldman Sachs at TBV

银行股Q3季报:JPMorgan目标价$100, Goldman Sachs关注Tangible Book Value

Summary

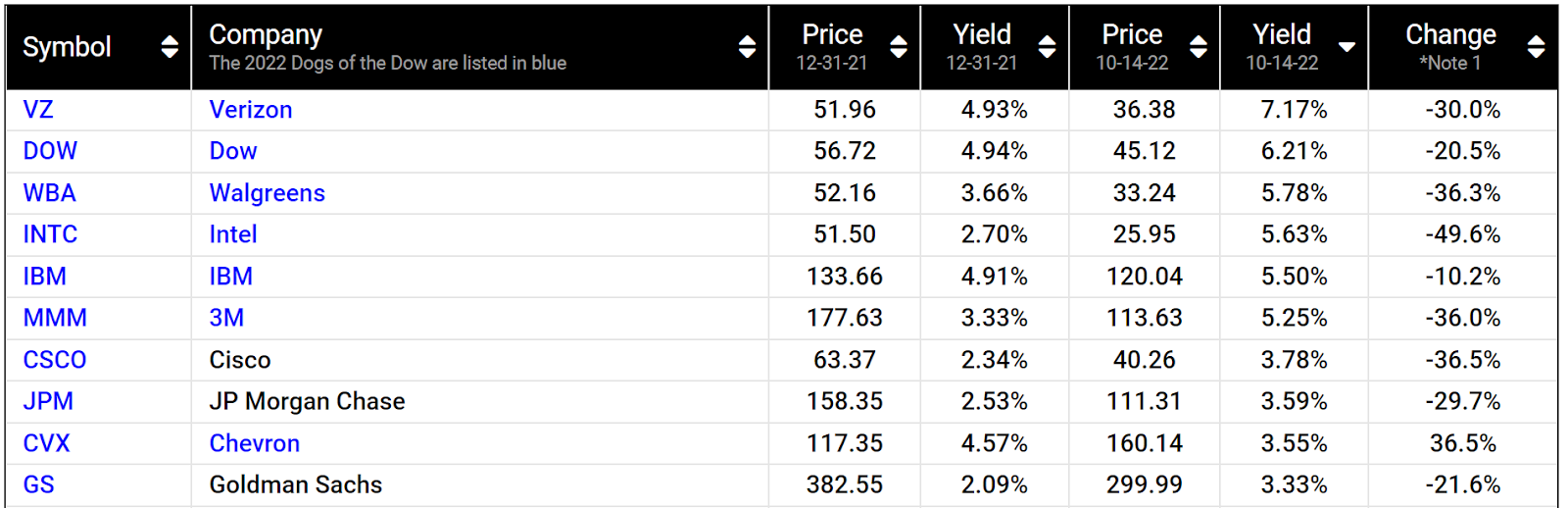

银行通常不会进入Dogs of the Dow。然而,本月,摩根大通和高盛目前是Dow list名单中收益率最高的第8和第10只股票。第三季度的盈利季节可能会使这两只股票处于多年来有吸引力的入门水平。持续的波动可能为高盛提供明确的账面价值,而摩根大通则将接近100美元的目标价。

Banks typically do not make it to the Dogs of the Dow list. However, this month, JPMorgan and Goldman Sachs are currently the 8th and 10th highest-yielding stocks in the Dow list. The Q3 earning season could offer both at multi-year attractive entry levels. The ongoing volatility might offer Goldman Sachs a tangible book value and JPMorgan near a target price of ~$100.

Thesis

Banks typically do not make it to the Dogs of the Dow list. However, this month, JPMorgan and Goldman Sachs are currently the 8th and 10th highest-yielding stocks in the Dow list as you can see from the following chart.

Q3 may offer GS at TBV

Buying good banks (such as GS and JPM) at or near tangible book value has been proven to be very successful investment in our experiences – for obvious reasons. We are only paying for the tangible book and getting everything else (such as future earning power) for free.

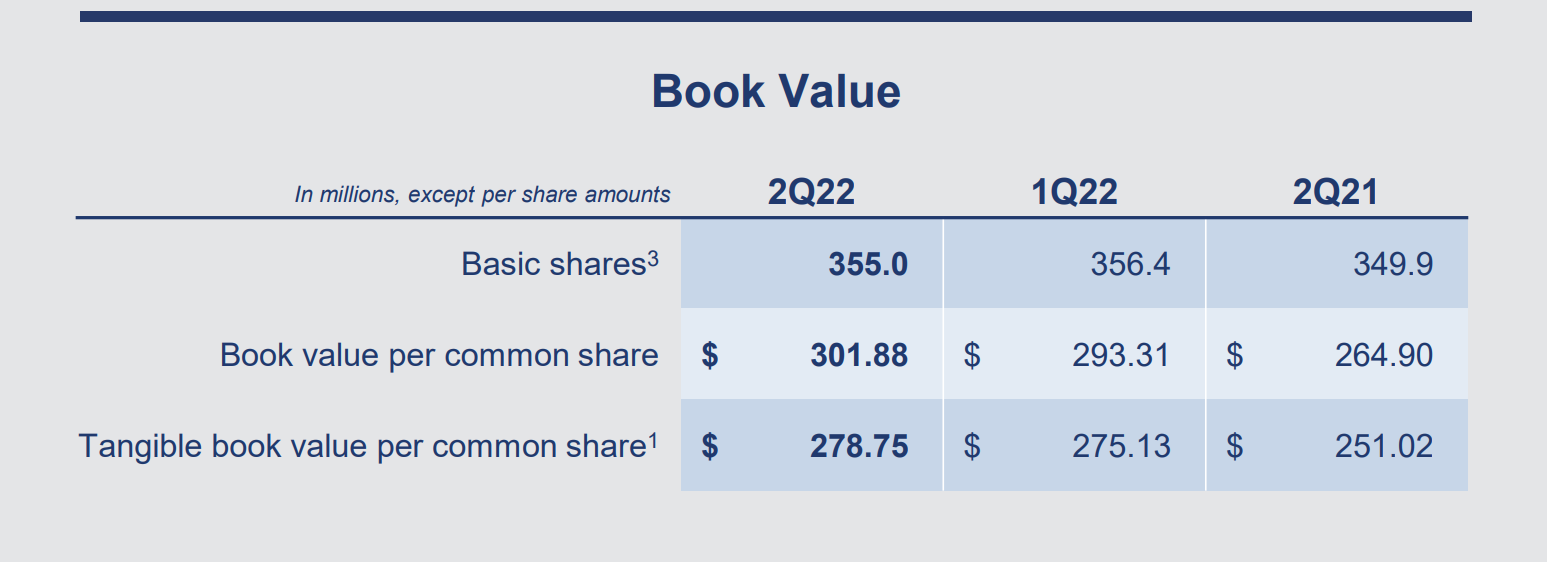

Although, readers have to be aware that book value is a moving target itself. When GS announced its Q1 book value of $293 per share and $301 per share in Q2, the number was delayed already, and it keep changing with market conditions. But historically, the price of GS is high so I suppose its stock price moves more than the book value as I’ve argued in an earlier article, creating buying/selling opportunities.

The volatility created in Q3 may create even large discounts so the stock may be offered near its tangible book value (“TBV”)

JPM target price of $100

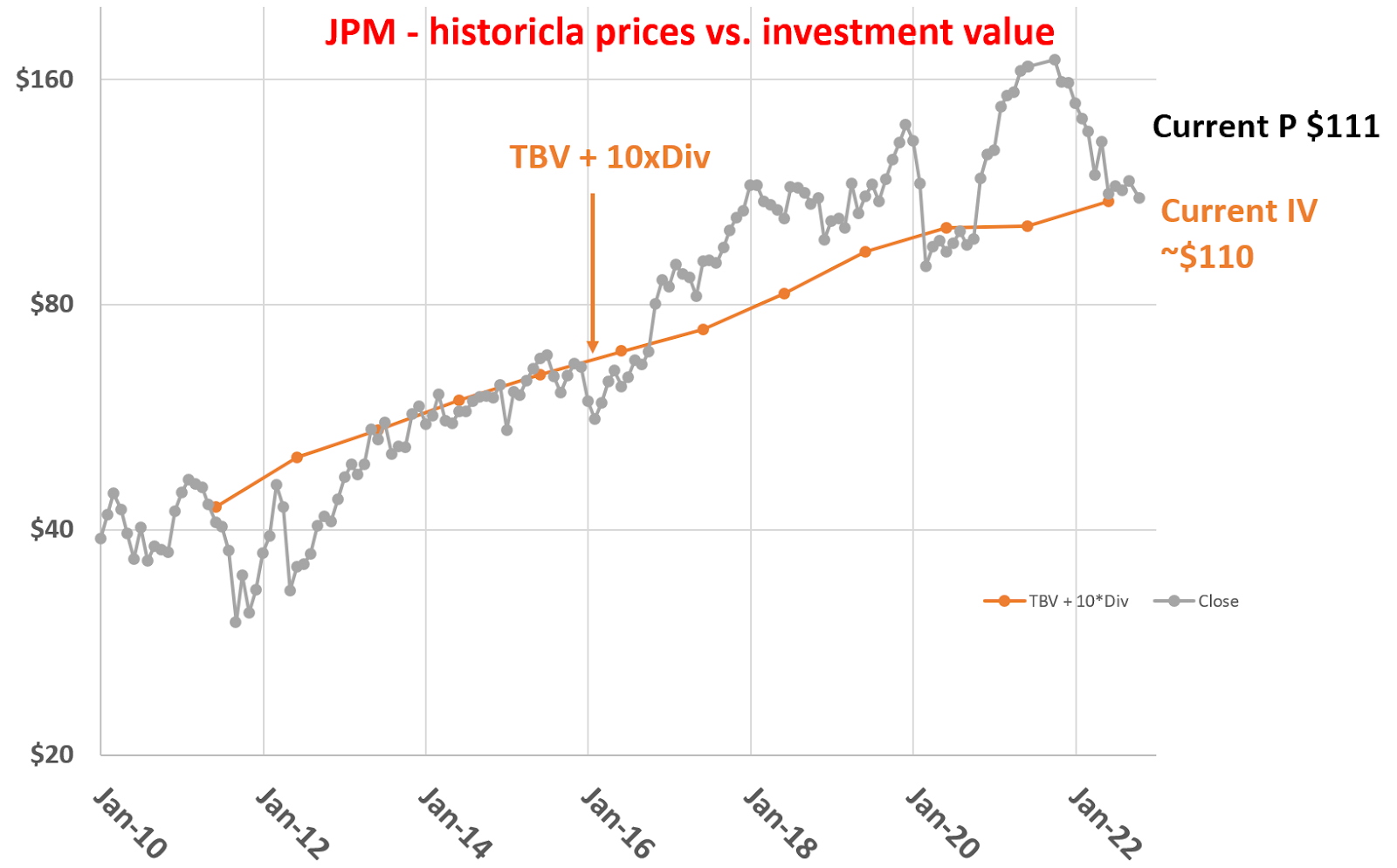

For an integrated bank like JPM, it is rarely for sale at tangible book value (or even just book value). Investors are willing to pay a premium for the extra safety enabled by its diversified revenue. The logical question is then: how much premium should we pay for JPM? A very intuitive and effective approach that we use ourselves for banking and REIT stocks is to add 10 times its dividend income to the TBV. The details are provided in my earlier articles.

The following chart shows the results of this method applied to JPM since 2010. As you can see, its latest TBV reported from its Q3 earnings is $69.9 per share (see the second chart below). With its $4 annual dividend per share, the IV works out to be about $118. To leave some margin of safety, we are targeting an entry price of $100 (to allow about ~10% of margin of safety).

If you liked these analyses, you can check out our other articles and join our chat group. We provide real time trade alerts, watchlist update, and portfolio adjustments in our chat groups

Follow us on Telegram channel to get the latest updates:

Or join our WeChat group for the latest news:

Full list of our articles and services:

Our websites: https://envisionret.myshopify.com/

Our past posts: https://seekingalpha.com/checkout?service_id=mp_1400